Strong operating results on core business. Record sales of loans. Financial results lower due to provisions for FX loans

Consolidated results of Bank Millennium Capital Group in 1st half of 2021.

Consolidated net profit of Bank Millennium Group after 2 quarters of 2021 reached -512 mln PLN (-200 mln PLN in Q2). The main factor weighing down on the results were provisions for legal risk involved with the portfolio of FX mortgages in the amount of 1 047 mln PLN (514 mln PLN in Q2). Were it not for the FX provisions the Group would have recorded net profit of 449 mln PLN (267 mln PLN in Q2 alone). The Bank had record-high sales of mortgage and cash loans at 4,8 bn PLN (+68% y/y) and 2,7 bn PLN (+14% y/y) respectively.

– Results after the 1st half of 2021 are clear proof that the Bank successfully mitigated most of the direct and indirect effects of the pandemic. Net profit before write-offs for legal risk involved with the portfolio of FX mortgages was 449 mln PLN. I also have a positive opinion about business results. The successful two quarters were above all about lending growth over the market (+6% y/y). A key role was played here by loans offered to retail customers. Sales of mortgages reached the record level of 4,8 bn PLN (+68% y/y), with cash loan sales at 2,7 bn PLN (+14% y/y). The number of active digital customers exceeded 2,7 million (14% growth y/y), while there were 2,14 million mobile customers (9% growth) – Joao Bras Jorge, Chairman of the Management Board of Bank Millennium, said summing-up the results. – In quarterly terms there was also 2% increase of the portfolio of corporate banking loans as well as strong recovery in leasing (+30% new sales volumes).

Main financial and business achievements of the group

2Q21 results were a clear proof that the BM Group successfully mitigated most of the direct and indirect impacts of the pandemic. 2Q21 pre-provision profit amounted to record PLN490 million and was 8% above the result in 2Q20 (1H21: PLN909 million, +6% y/y).

The improvement was driven by positive operating jaws – revenues grew 1% y/y (y/y dynamic of NII turned positive, y/y fee growth accelerated to 17%) while opex (ex-BFG) was down 7% (1H21: -11%) owing to savings in both staff (2Q21: -1% y/y, 1H21: -9% y/y) and non-staff costs (2Q21: -15%, 1H21: -13%). BFG charges which in 1H21 were 26% lower than in the same period last year provided an additional support.

The key developments in the last twelve months that drove the y/y improvement of the results and which, we believe, are particularly worth highlighting are as follows:

- recovery of NII to above 2Q20 level;

- rebound of quarterly NIM to 260bps in 2Q21, just 39bps below the 2019 peak (299bps in 3Q19) and 11bps up from the low of 249bps in 3Q20;

- strong reduction of deposit cost (down 100bps since YE19) to 7bps in 2Q21 was among the key drivers;

- above-market loan growth (+6% y/y) despite accelerating reduction of the FX-mortgage portfolio; a steady uptrend in retail loan originations played a key role – disbursements of mortgages in 2Q21 reached a new quarterly record of PLN2.6bn, up 71% y/y (1H21: PLN4.8bn, up 68% y/y) translating into market share of 12% vs. 13% in 2Q20 while 2Q21 origination of cash loans reached a record PLN1.4bn, up 33% y/y (1H21: PLN2.7bn, up 14% y/y); on a separate count our FX-mortgage book contracted 21% y/y due to a combination of repayments, provisioning (most of legal risk provisions are booked against gross value of loans under court proceedings) and conversions to PLN negotiated between the Bank and the borrowers; as a result, the share of FX-mortgages in total gross loans decreased to 15.1% (BM originated only: 13.9%) from 20.3% (18.9%) in the same period last year.

- improving cost efficiency owing to a combination of a steady increase in the digitalisation of our business and well as relations with clients with strong cost response to revenue pressures; falling headcount (number of active employees down 881 or 12% since 2Q20), ongoing optimisation of our physical distribution network (own branches down by 90 units or 17% in the last twelve months) complimented the increasing share of digital services (digital customers: 2.14 million, up 9% y/y, number of active mobile customers: 1.8 million, up 15% y/y); cost optimisation initiatives not only resulted nominal reduction of opex but also translated into much improved cost efficiency; reported C/I ratio declined to 41% in 2Q21 from 47% in the same period last year (C/I ratio excluding BFG and netting-off of FX mortgage provisions on f.EB book fell to 40% from 44%), cost/asset ratio declined to 1.5% from 1.6% while opex per employee fell to PLN54,000 in 1H21 from around 57,000 in 1H20);

- stable loan book quality resulting in a low cost of risk (28bps in 2Q21 vs. 121bps in 2Q20) with positive underlying trends in quality of both retail and corporate books and continued NPL disposals; NPL ratio declined to 4.7% at the end of June’21 from nearly 4.9% the year before;

- AuM of Millennium TFI and third party funds combined grew 5% q/q to over PLN9.4 billion with y/y growth at 32%.

Strategy implementation

Given the unprecedented scale of change of the business environment caused by the outbreak of COVID-19 pandemic in early 2020 the BM Group decided to extend its 2018-20 strategy by additional year and prepare a new one for the years 2022-2024.

The Bank aims to recover like-for-like operational results affected by the COVID-19 crisis and its direct and indirect consequences within 1.5 to 2 years. This is to be achieved by completion of the current cost streamlining program, introduction of new operational efficiency program as well as an improvement business results through improved pricing and sales increase in core products.

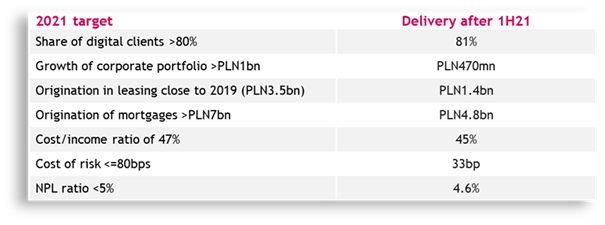

The Group is on well on track to deliver on its 2021 targets:

Results of the Group are also available here: https://www.bankmillennium.pl/o-banku/relacje-inwestorskie

Author:

Bank Millennium

Last Updated on August 2, 2021 by Karolina Ampulska