Cushman & Wakefield predicts Sheds, Beds & Meds will be 2021 investment winners

“Sheds, Beds, Meds” and other alternative market sectors will dominate the EMEA investment agenda this year, as investors remain risk averse, focusing on core markets with better long-term growth prospects until the economic impact of COVID-19 abates. These findings form part of ‘The Signal Report: Investor’s Quarterly Guide to 2021’, the latest global investment insights from leading real estate firm Cushman & Wakefield.

- Alternatives to stay on top as structural changes and COVID legacies affect how we live, work and play

- Investors to lead road to recovery as low interest rates, abundant liquidity and a lack of options drive demand

- EMEA investment activity expected to pick up in H2 2021, with sustainability rising up the agenda

Alternatives continue to outperform

Cushman & Wakefield predicts Logistics, Residential and Life Sciences (or “Sheds, Beds & Meds”) will benefit significantly from the lifestyle shifts caused by the pandemic, with changing working, living and shopping patterns continuing to disrupt the status quo. Likewise, other alternative assets such as data centres and self-storage are expected to continue a trajectory of strong growth this year.

Repurposing existing assets is also a major area of opportunity, including mixed-use and specific sector prospects such as supporting click and collect and “last metre” inner urban logistics and evolving areas of tech infrastructure.

David Hutchings, Head of Investment Strategy, EMEA Capital Markets at Cushman & Wakefield and report author, said: “Investment activity across EMEA markets closely rests on wider economic recovery and easing of Covid-19 restrictions, which continues to dictate investor appetite and the performance of specific sectors. Asia and North America will lead the global economic upturn, but European growth is also set to accelerate later in the year. Nonetheless, amidst ongoing structural changes in how we use offices and shops in particular, it will be logistics and alternatives such as residential to rent, health and life sciences which will retain their title as pandemic ‘winners’ this year.”

Office and retail transformation

Meanwhile, office and retail activity is expected to pick up in H2 2021 once vaccination rates have increased and Covid-19 restrictions are eased. Assets in these sectors will be impacted by quality of location and sense of destination, influencing tenant demand and ultimately pricing.

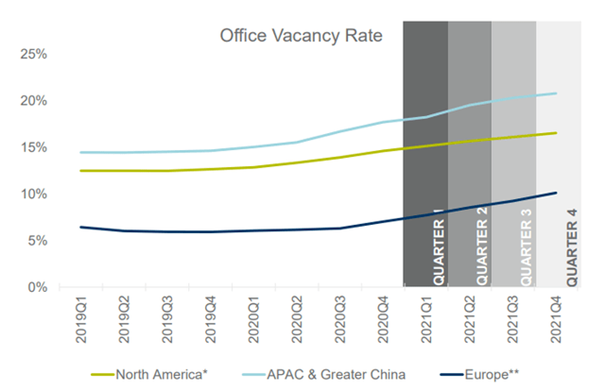

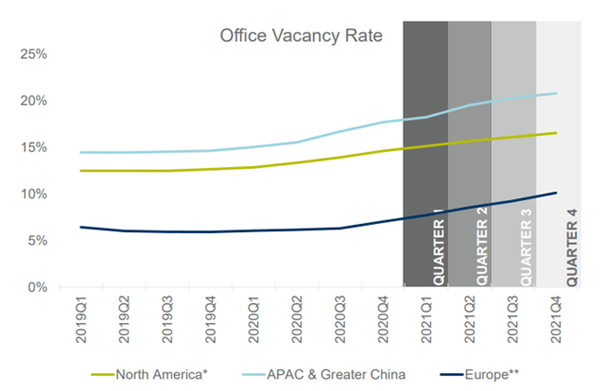

EMEA is expected to maintain the lowest office vacancy rate throughout 2021, with a modest and steady increase reaching just shy of 10% by Q4 2021, largely due to long lease lengths commitments and a restricted development pipeline. Vacancy rates in North America and APAC & Greater China, are expected to reach in between 15-20% by the final quarter of the year.

Hutchings said: “Office and retail should not be overlooked, especially as office workers return to the workplace and non-essential retail opens back up over Q2 and Q3. The pandemic has undoubtedly brought quality of location and wider placemaking to the forefront and these factors will be critical to meeting occupier demand. Instead of looking at these sectors in isolation, investors may find success in taking a more holistic approach and exploring the potential for mixed-use, again helping to create a destination and sense of place.”

Figure 2: Global office vacancy rate

Source: Cushman & Wakefield Research. Note: *Excludes Mexico. **Excludes Russia and Turkey.

Slower leasing market recovery in EMEA

While investors will be on the front foot once conditions allow, occupier recovery will be more protracted. Renewed lockdown restrictions in late 2020, a structurally slower-to-adjust labour market and generally slow vaccination rates (minus the UK and Israel), have dampened occupier recovery in the near term, with 1.3 million job losses expected across the region in 2021. Therefore, activity isn’t anticipated to significantly pick up until H2 2021.

Even then however the recovery in western Europe will be more gradual than in other global markets. Analysis of the impact of COVID-19 on real GDP levels shows European nations amongst the slowest to recover. Within a global ranking of the 20 largest economies, the UK, France and Spain can expect the longest recovery times, from 2022 Q4 for the UK to 2023 Q4 for Spain. This is significantly longer than Mainland China, Taiwan and Australia at the top of the ranking, whose GDPs surpassed pre-COVID levels back in the middle of 2020.

European investor demand continues to be largely focused on core countries, but the rapid economic bounce back forecast in areas such as Poland will encourage more to shift their focus and explore new opportunities.

Figure 1: Recovery of major global economies

Source: Various government agencies, Moody’s Analytics, Cushman & Wakefield Research.

Global outlook for 2021

The road to recovery looks uneven but will be led by investors as low interest rates, abundant liquidity and a lack of alternative investment options drive demand. This differs at regional level as conditions are consistently more positive in the Asia Pacific region followed by North America, while Europe, Latin America and emerging markets generally lagging. However, all regions are expected to end 2021 with strong momentum.

David Hutchings, Head of Investment Strategy, EMEA Capital Markets at Cushman & Wakefield and author of the report, concluded: “As with 2020, global economies, leasing markets and capital markets will march to the tune of the pandemic situation, which is clearly impacting regions differently. Investors need to look way beyond the current short-term cycle to make the best investment decisions, with structural changes driving performance, led by digital transformation but with environmental sustainability a close rival as far as European players are concerned. For the short term, our analysis suggests H2 2021 is when we’ll start to see real momentum build across all markets, Pent-up demand and an extremely permissive financial environment could in fact create a ‘sugar-high’ boosted economic recovery in Q4, resulting in an extremely dynamic market at year’s end.”

Author:

Cushman & Wakefield

Last Updated on March 11, 2021 by Karolina Ampulska